The Hows and Whys of Gold Price Manipulation

By: Paul Craig Roberts and Dave Kranzler

January 17, 2014

visit www.paulcraigroberts.org for more

The deregulation of the financial system during the Clinton and George W. Bush regimes had the predictable result: financial concentration and reckless behavior. A handful of banks grew so large that financial authorities declared them “too big to fail.” Removed from market discipline, the banks became wards of the government requiring massive creation of new money by the Federal Reserve in order to support through the policy of Quantitative Easing the prices of financial instruments on the banks’ balance sheets and in order to finance at low interest rates trillion dollar federal budget deficits associated with the long recession caused by the financial crisis.

The deregulation of the financial system during the Clinton and George W. Bush regimes had the predictable result: financial concentration and reckless behavior. A handful of banks grew so large that financial authorities declared them “too big to fail.” Removed from market discipline, the banks became wards of the government requiring massive creation of new money by the Federal Reserve in order to support through the policy of Quantitative Easing the prices of financial instruments on the banks’ balance sheets and in order to finance at low interest rates trillion dollar federal budget deficits associated with the long recession caused by the financial crisis.

The Fed’s policy of monetizing one trillion dollars of bonds annually put pressure on the US dollar, the value of which declined in terms of gold. When gold hit $1,900 per ounce in 2011, the Federal Reserve realized that $2,000 per ounce could have a psychological impact that would spread into the dollar’s exchange rate with other currencies, resulting in a run on the dollar as both foreign and domestic holders sold dollars to avoid the fall in value. Once this realization hit, the manipulation of the gold price moved beyond central bank leasing of gold to bullion dealers in order to create an artificial market supply to absorb demand that otherwise would have pushed gold prices higher. The manipulation consists of the Fed using bullion banks as its agents to sell naked gold shorts in the New York Comex futures market. Short selling drives down the gold price, triggers stop-loss orders and margin calls, and scares participants out of the gold trusts. The bullion banks purchase the deserted shares and present them to the trusts for redemption in bullion. The bullion can then be sold in the London physical gold market, where the sales both ratify the lower price that short-selling achieved on the Comex floor and provide a supply of bullion to meet Asian demands for physical gold as opposed to paper claims on gold.

Tonnage of Gold is moving to Asia

The evidence of gold price manipulation is clear. In this article we present evidence and describe the process. We conclude that ability to manipulate the gold price is disappearing as physical gold moves from New York and London to Asia, leaving the West with paper claims to gold that greatly exceed the available supply.

Courtesy Comex

The primary venue of the Fed’s manipulation activity is the New York Comex exchange, where the world trades gold futures. Each gold futures contract represents one gold 100 ounce bar. The Comex is referred to as a paper gold exchange because of the use of these futures contracts. Although several large global banks are trading members of the Comex, JP Morgan, HSBC and Bank Nova Scotia conduct the majority of the trading volume. Trading of gold (and silver) futures occurs in an auction-style market on the floor of the Comex daily from 8:20 a.m. to 1:30 p.m. New York time. Comex futures trading also occurs on what is known as Globex. Globex is a computerized trading system used for derivatives, currency and futures contracts. It operates continuously except on weekends. Anyone anywhere in the world with access to a computer-based futures trading platform has access to the Globex system.

In addition to the Comex, the Fed also engages in manipulating the price of gold on the far bigger–in terms of total dollar value of trading–London gold market. This market is called the LBMA (London Bullion Marketing Association) market. It is comprised of several large banks who are LMBA market makers known as “bullion banks” (Barclays, Credit Suisse, Deutsche Bank, Goldman Sachs, HSBC, JPMorganChase, Merrill Lynch/Bank of America, Mitsui, Societe Generale, Bank of Nova Scotia and UBS). Whereas the Comex is a “paper gold” exchange, the LBMA is the nexus of global physical gold trading and has been for centuries. When large buyers like Central Banks, big investment funds or wealthy private investors want to buy or sell a large amount of physical gold, they do this on the LBMA market.

1.2 Million Ounces of Gold in less than 60 seconds

The Fed’s gold manipulation operation involves exerting forceful downward pressure on the price of gold by selling a massive amount of Comex gold futures, which are dropped like bombs either on the Comex floor during NY trading hours or via the Globex system. A recent example of this occurred on Monday, January 6, 2014. After rallying over $15 in the Asian and European markets, the price of gold suddenly plunged $35 at 10:14 a.m. In a space of less than 60 seconds, more than 12,000 contracts traded – equal to more than 10% of the day’s entire volume during the 23 hour trading period in which which gold futures trade. There was no apparent news or market event that would have triggered the sudden massive increase in Comex futures selling which caused the sudden steep drop in the price of gold. At the same time, no other securities market (other than silver) experienced any unusual price or volume movement. 12,000 contracts represents 1.2 million ounces of gold, an amount that exceeds by a factor of three the total amount of gold in Comex vaults that could be delivered to the buyers of these contracts.

This manipulation by the Fed involves the short-selling of uncovered Comex gold futures. “Uncovered” means that these are contracts that are sold without any underlying physical gold to deliver if the buyer on the other side decides to ask for delivery. This is also known as “naked short selling.” The execution of the manipulative trading is conducted through one of the major gold futures trading banks, such as JPMorganChase, HSBC, and Bank of Nova Scotia. These banks do the actual selling on behalf of the Fed. The manner in which the Fed dumps a large quantity of futures contracts into the market differs from the way in which a bona fide trader looking to sell a big position would operate. The latter would try to work off his position carefully over an extended period of time with the goal of trying to disguise his selling and to disturb the price as little as possible in order to maximize profits or minimize losses. In contrast, the Fed‘s sales telegraph the intent to drive the price lower with no regard for preserving profits or fear or incurring losses, because the goal is to inflict as much damage as possible on the price and intimidate potential buyers.

Globex System Manipulated by Fed

The Fed also actively manipulates gold via the Globex system. The Globex market is punctuated with periods of “quiet” time in which the trade volume is very low. It is during these periods that the Fed has its agent banks bombard the market with massive quantities of gold futures over a very brief period of time for the purpose of driving the price lower. The banks know that there are very few buyers around during these time periods to absorb the selling. This drives the price lower than if the selling operation occurred when the market is more active.

The Fed also actively manipulates gold via the Globex system. The Globex market is punctuated with periods of “quiet” time in which the trade volume is very low. It is during these periods that the Fed has its agent banks bombard the market with massive quantities of gold futures over a very brief period of time for the purpose of driving the price lower. The banks know that there are very few buyers around during these time periods to absorb the selling. This drives the price lower than if the selling operation occurred when the market is more active.

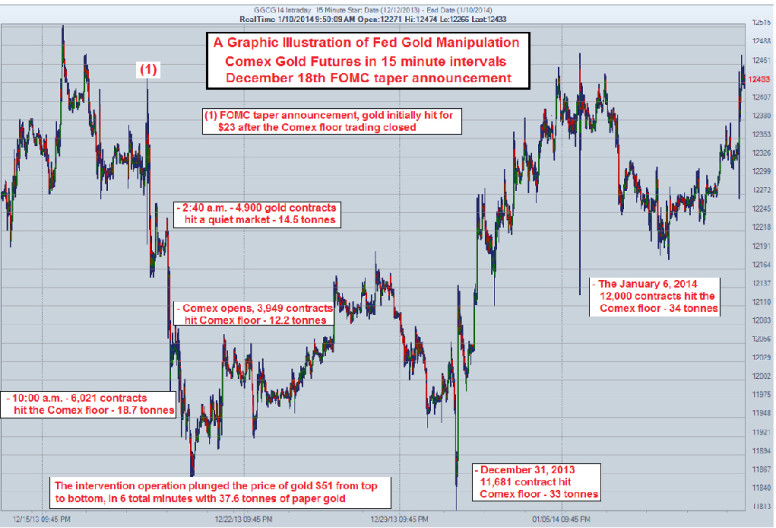

A primary example of this type of intervention occurred on December 18, 2013, immediately after the FOMC announced its decision to reduce bond purchases by $10 billion monthly beginning in January 2014. With the rest of the trading world closed, including the actual Comex floor trading, a massive amount of Comex gold futures were sold on the Globex computer trading system during one of its least active periods. This selling pushed the price of gold down $23 dollars in the space of two hours. The next wave of futures selling occurred in the overnight period starting at 2:30 a.m. NY time on December 19th. This time of day is one of the least active trading periods during any 23 hour trading day (there’s one hour when gold futures stop trading altogether). Over 4900 gold contracts representing 14.5 tonnes of gold were dumped into the Globex system in a 2-minute period from 2:40-2:41 a.m, resulting in a $24 decline in the price of gold. This wasn’t the end of the selling. Shortly after the Comex floor opened later that morning, another 1,654 contracts were sold followed shortly after by another 2,295 contracts. This represented another 12.2 tonnes of gold. Then at 10:00 a.m. EST, another 2,530 contracts were unloaded on the market followed by an additional 3,482 contracts just six minutes later. These sales represented another 18.7 tonnes of gold.

All together, in 6 minutes during an eight hour period, a total amount of 37.6 tonnes (a “tonne” is a metric ton–about 10% more weight than a US ”ton”) of gold future contracts were sold. The contracts sold during these 6 minutes accounted for 10% of the total volume during that 23 hours period of time. Four-tenths of one percent of the trading day accounted for 10% of the total volume. The gold represented by the futures contracts that were sold during these 6 minutes was a multiple of the amount of physical gold available to Comex for delivery.

The purpose of driving the price of gold down was to prevent the announced reduction in bond purchases (the so-called tapering) from sending the dollar, stock and bond markets down. The markets understand that the liquidity that Quantitative Easing provides is the reason for the high bond and stock prices and understand also that the gains from the rising stock market discourage gold purchases. Previously when the Fed had mentioned that it might reduce bond purchases, the stock market fell and bonds sold off. To neutralize the market scare, the Fed manipulated both gold and stock markets. (See Pam Martens for explanation of the manipulation of the stock market: http://wallstreetonparade.com/2013/12/why-didn’t-the-stock-market-sell-off-on-the-fed’s-taper-announcement/ )

While the manipulation of the gold market has been occurring since the start of the bull market in gold in late 2000, this pattern of rampant manipulative short-selling of futures contracts has been occurring on a more intense basis over the last 2 years, during gold’s price decline from a high of $1900 in September 2011. The attack on gold’s price typically will occur during one of several key points in time during the 23 hour Globex trading period. The most common is right at the open of Comex gold futures trading, which is 8:20 a.m. New York time. To set the tone of trading, the price of gold is usually knocked down when the Comex opens. Here are the other most common times when gold futures are sold during illiquid Globex system time periods:

– 6:00 p.m NY time weekdays, when the Globex system re-opens after closing for an hour;

– 6:00 p.m. Sunday evening NY time when Globex opens for the week;

– 2:30 a.m. NY time, when Shanghai Gold Exchange closes

– 4:00 a.m. NY time, just after the morning gold “fix” on the London gold market (LBMA);

2:00 p.m. NY time any day but especially on Friday, after the Comex floor trading has closed – it’s an illiquid Globex-only session and the rest of the world is still closed.

In addition to selling futures contracts on the Comex exchange in order to drive the price of gold lower, the Fed and its agent bullion banks also intermittently sell large quantities of physical gold in London’s LBMA gold market. The process of buying and selling actual physical gold is more cumbersome and complicated than trading futures contracts. When a large supply of physical gold hits the London market all at once, it forces the market a lot lower than an equivalent amount of futures contracts would. As the availability of large amounts of physical gold is limited, these “physical gold drops” are used carefully and selectively and at times when the intended effect on the market will be most effective.

The primary purpose for short-selling futures contracts on Comex is to protect the dollar’s value from the growing supply of dollars created by the Fed’s policy of Quantitative Easing. The Fed’s use of gold leasing to supply gold to the market in order to reduce the rate of rise in the gold price has drained the Fed’s gold holdings and is creating a shortage in physical gold. Historically most big buyers would leave their gold for safe-keeping in the vaults of the Fed, Bank of England or private bullion banks rather than incur the cost of moving gold to local depositories. However, large purchasers of gold, such as China, now require actual delivery of the gold they buy.

LBMA

Demands for gold delivery have forced the use of extraordinary and apparently illegal tactics in order to obtain physical gold to settle futures contracts that demand delivery and to be able to deliver bullion purchased on the London market (LBMA). Gold for delivery is obtained from opaque Central Bank gold leasing transactions, from “borrowing” client gold held by the bullion banks like JP Morgan in their LBMA custodial vaults, and by looting the gold trusts, such as GLD, of their gold holdings by purchasing large blocks of shares and redeeming the shares for gold.

Central Bank gold leasing occurs when Central Banks take physical gold they hold in custody and lease it to bullion banks. The banks sell the gold on the London physical gold market. The gold leasing transaction makes available physical gold that can be delivered to buyers in quantities that would not be available at existing prices. The use of gold leasing to manipulate the price of gold became a prevalent practice in the 1990’s. While Central Banks admit to engaging in gold lease transactions, they do not admit to its purpose, which is to moderate rises in the price of gold, although Fed Chairman Alan Greenspan did admit during Congressional testimony on derivatives in 1998 that “Central banks stand ready to lease gold in increasing quantities should the price rise.”

Another method of obtaining bullion for sale or delivery is known as “rehypothecation.” Rehypothecation occurs when a bank or brokerage firm “borrows” client assets being held in custody by banks. Technically, bank/brokerage firm clients sign an agreement when they open an account in which the assets in the account might be pledged for loans, like margin loans. But the banks then take pledged assets and use them for their own purpose rather than the client’s. This is rehypothecation. Although Central Banks fully disclose the practice of leasing gold, banks/brokers do not publicly disclose the details of their rehypothecation activities.

Over the course of the 13-year gold bull market, gold leasing and rehypothecation operations have largely depleted most of the gold in the vaults of the Federal Reserve, Bank of England, European Central Bank and private bullion banks such as JPMorganChase. The depletion of vault gold became a problem when Venezuela was the first country to repatriate all of its gold being held by foreign Central Banks, primarily the Fed and the BOE. Venezuela’s request was provoked by rumors circulating the market that gold was being leased and hypothecated in increasing quantities. About a year later, Germany made a similar request. The Fed refused to honor Germany’s request and, instead, negotiated a seven year timeline in which it would ship back 300 of Germany’s 1500 tonnes. This made it apparent that the Fed did not have the gold it was supposed to be holding for Germany.

Deutsche Bundesbank wants their gold back.

Why does the Fed need seven years in which to return 20 percent of Germany’s gold? The answer is that the Fed does not have the gold in its vault to deliver. In 2011 it took four months to return Venezuela’s 160 tonnes of gold. Obviously, the gold was not readily at hand and had to be borrowed, perhaps from unsuspecting private owners who mistakenly believe that their gold is held in trust.

Paper Claims to Actual Gold: 93 to 1

Western central banks have pushed fractional gold reserve banking to the point that they haven’t enough reserves to cover withdrawals. Fractional reserve banking originated when medieval goldsmiths learned that owners of gold stored in their vault seldom withdrew the gold. Instead, those who had gold on deposit circulated paper claims to gold. This allowed goldsmiths to lend gold that they did not have by issuing paper receipts. This is what the Fed has done. The Fed has created paper claims to gold that does not exist in physical form and sold these claims in mass quantities in order to drive down the gold price. The paper claims to gold are a large multiple of the amount of actual gold available for delivery. The Reserve Bank of India reports that the ratio of paper claims to gold exceed the amount of gold available for delivery by 93:1.

Fractional reserve systems break down when too many depositors or holders of paper claims present them for delivery. Breakdown is occurring in the Fed’s fractional bullion operation. In the last few years the Asian markets–specifically and especially the Chinese–are demanding actual physical delivery of the bullion they buy. This has created a sense of urgency among the Fed, Treasury and the bullion banks to utilize any means possible to flush out as many weak holders of gold as possible with orchestrated price declines in order to acquire physical gold that can be delivered to Asian buyers

The $650 decline in the price of gold since it hit $1900 in September 2011 is the result of a manipulative effort designed both to protect the dollar from Quantitative Easing and to free up enough gold to satisfy Asian demands for delivery of gold purchases.

Around the time of the substantial drop in gold’s price in April, 2013, the Bank of England’s public records showed a 1300 tonne decline in the amount of gold being held in the BOE bullion vaults. This is a fact that has not been denied or reasonably explained by BOE officials despite several published inquiries. This is gold that was being held in custody but not owned by the Bank of England. The truth is that the 1300 tonnes is gold that was required to satisfy delivery demands from the large Asian buyers. It is one thing for the Fed or BOE to sell, lease or rehypothecate gold out of their vault that is being safe-kept knowing the entitled owner likely won’t ask for it anytime soon, but it is another thing altogether to default on a gold delivery to Asians demanding delivery.

Default on delivery of purchased gold would terminate the Federal Reserve’s ability to manipulate the gold price. The entire world would realize that the demand for gold greatly exceeds the supply, and the price of gold would explode upwards. The Federal Reserve would lose control and would have to abandon Quantitative Easing. Otherwise, the exchange value of the US dollar would collapse, bringing to an end US financial hegemony over the world.

Last April, the major takedown in the gold price began with Goldman Sachs issuing a “technical analysis” report with an $850 price target (gold was around $1650 at that time). Goldman Sachs also broadcast to every major brokerage firm and hedge fund in New York that gold was going to drop hard in price and urged brokers to get their clients out of all physical gold holdings and/or shares in physical gold trusts like GLD or CEF. GLD and CEF are trusts that purchase physical gold/silver bullion and issue shares that represent claims on the bullion holdings. The shares are marketed as investments in gold, but represent claims that can only be redeemed in very large blocks of shares, such as 100,000, and perhaps only by bullion banks. GLD is the largest gold ETF (exchange traded firm), but not the only one. The purpose of Goldman Sachs’ announcement was to spur gold sales that would magnify the price effect of the short-selling of futures contracts. Heavy selling of futures contracts drove down the gold price and forced sales of GLD and other ETF shares, which were bought up by the bullion banks and redeemed for gold

At the beginning of 2013, GLD held 1350 tonnes of gold. By April 12th, when the heavy intervention operation began, GLD held 1,154 tonnes. After the series of successive raids in April, the removal of gold from GLD accelerated and currently there are 793 tonnes left in the trust. In a little more than one year, more than 41% of the gold bars held by GLD were removed – most of that after the mid-April intervention operation.

In addition, the Bank of England made its gold available for purchase by the bullion banks in order to add to the ability to deliver gold to Asian purchasers.

The financial media, which is used to discredit gold as a safe haven from the printing of fiat currencies, claims that the decline in GLD’s physical gold is an indication that the public is rejecting gold as an investment. In fact, the manipulation of the gold price downward is being done systematically in order to coerce holders of GLD to unload their shares. This enables the bullion banks to accumulate the amount of shares required to redeem gold from the GLD Trust and ship that gold to Asia in order to meet the enormous delivery demands. For example, in the event described above on January 6th, 14% of GLD’s total volume for the day traded in a 1-minute period starting at 10:14 a.m. The total volume on the day for GLD was almost 35% higher than the average trading volume in GLD over the previous ten trading days

Before 2013, the amount of gold in the GLD vault was one of the largest stockpiles of gold in the world. The swift decline in GLD’s gold inventory is the most glaring indicator of the growing shortage of physical gold supply that can be delivered to the Asian market and other large physical gold buyers. The more the price of gold is driven down in the Western paper gold market, the higher the demand for physical bullion in Asian markets. In addition, several smaller physical gold ETFs have experienced substantial gold withdrawals. Including the more than 100 tonnes of gold that has disappeared from the Comex vaults in the last year, well over 1,000 tonnes of gold has been removed from the various ETFs and bank custodial vaults in the last year. Furthermore, there is no telling how much gold that is kept in bullion bank private vaults on behalf of wealthy investors has been rehypothecated. All of this gold was removed in order to avoid defaulting on delivery demands being imposed by Asian commercial, investment and sovereign gold buyers.

The Federal Reserve seems to be trapped. The Fed is creating approximately 1,000 billion new US dollars annually in order to support the prices of debt related derivatives on the books of the few banks that have been declared to be “to big to fail” and in order to finance the large federal budget deficit that is now too large to be financed by the recycling of Chinese and OPEC trade surpluses into US Treasury debt. The problem with Quantitative Easing is that the annual creation of an enormous supply of new dollars is raising questions among American and foreign holders of vast amounts of US dollar-denominated financial instruments. They see their dollar holdings being diluted by the creation of new dollars that are not the result of an increase in wealth or GDP and for which there is no demand

Quantitative Easing is a threat to the dollar’s exchange value. The Federal Reserve, fearful that the falling value of the dollar in terms of gold would spread into the currency markets and depreciate the dollar, decided to employ more extreme methods of gold price manipulation.

When gold hit $1,900, the Federal Reserve panicked. The manipulation of the gold price became more intense. It became more imperative to drive down the price, but the lower price resulted in higher Asian demand for which scant supplies of gold were available to meet.

Having created more paper gold claims than there is gold to satisfy, the Fed has used its dependent bullion banks to loot the gold exchange traded funds (ETFs) of gold in order to avoid default on Asian deliveries. Default would collapse the fractional bullion system that allows the Fed to drive down the gold price and protect the dollar from QE.

What we are witnessing is our central bank pulling out all stops on integrity and lawfulness in order to serve a small handful of banks that financial deregulation allowed to become “too big to fail” at the expense of our economy and our currency. When the Fed runs out of gold to borrow, to rehypothecate, and to loot from ETFs, the Fed will have to abandon QE or the US dollar will collapse and with it Washington’s power to exercise hegemony over the world.

Dave Kranzler traded high yield bonds for Bankers Trust for a decade. As a co-founder and principal of Golden Returns Capital LLC, he manages the Precious Metals Opportunity Fund. Click Here to go to his website.